Tired of that massive amount of student loan debt? Ever wonder how it could be possible to pay off your loans in just a few years? Those who have done it will tell you, it’s not easy. If you’re facing a mountain of student loan bills and are looking for a way out, then you need to consider an option such as the Student Loan Consolidation Loan. It’s not a quick fix, but rather an opportunity to develop a new plan so that you can pay off your high interest rate student loans quickly and with reduced monthly payments . You’ll find information about what is allowed on the web site. In addition, you’ll also discover how much money you might save in the long run by simply comparing two scenarios:

In this article, you will learn about; 70000 student loan monthly payment, student loan payments and student loan amortization schedule. Other pieces of info like; loan repayment calculator, student loan monthly payment calculator, student loan repayment calculator based on income and many more are available on our website.

Have you ever been in a situation where you cannot pay your bills or make ends meet even if you worked hard? This is the situation that I was in. I had my friends but they could not be of any help since the debts and their resultant effects were not as severe as mine. From this experience I have come to learn that there are always people who can tell you some ways in which you can get out of your debt problem easily with minimum effort.

60000 in student loans monthly payment

Learn how to dramatically reduce your student loan payments.

If you still have a high payment on your student loans and are struggling to make ends meet, it may be time to consider refinancing them. We’ve helped thousands of borrowers lower their monthly payments and see less interest added to their total over time.

All you have to do is answer a few questions about your loan, and we’ll show you which lenders are willing to take you on as a client. You can then choose the lender that you think will give you the best deal, and start paying off your loans quickly!

We’re so glad you’ve chosen to make minimum payments on your student loans.

This is the first step to becoming debt free! In fact, depending on the payment options you choose, you can put yourself in an even better financial situation than before you took out your loans.

Many people who take out student loans are surprised by how much they owe after graduation. If they haven’t been making monthly payments during school, they may be overwhelmed when they start receiving bills for thousands of dollars.

Luckily, there are several ways to pay off your student loans. You can choose to make minimum payments or lump sum payments at any time. When you make a minimum payment, you’re only paying the interest on your loan. This means that although your balance will remain the same each month, it won’t go down until you begin making additional payments toward principal (the original amount borrowed).

If you decide to make lump sum payments, these will go toward both principal and interest. You may want to consider this option if you have extra money available from another source such as a bonus check or tax refund.

For example, let’s say there are two students: one who makes minimum payments and another who makes lump

If you have $60,000 in student loan debt and you’re making $40,000 a year, your monthly payments should be about $350. That’s assuming you’re on the standard 10-year repayment plan, of course. If you ever need to adjust those payments, it’s not hard to do. You can always refinance your loans or find a lower interest rate if your credit and income increase over time.

It’s important to keep track of how much you owe so that you don’t fall behind—and so that you can manage your payments appropriately. If you’re ever not sure what to do with your money, just remember: budgeting is important!

How to Pay Off $60K in Student Loans in 3 Years (While Making Only $30K)

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It may not have been reviewed, commissioned or otherwise endorsed by any of our network partners.

Note that the situation for student loans has changed due to the impact of the coronavirus outbreak and relief efforts from the government, student loan lenders and others. Check out our Student Loan Hero Coronavirus Information Center for additional news and details.

Most of us don’t learn how to pay off $60,000 or more in student loans in school. But you might find yourself managing debt of that magnitude, especially if you take out loans for both undergraduate and graduate school.

That was the case for Robbie Eleazer when he graduated from the Southern California Institute of Architecture (SCI-Arc) with $60,000 in student loans. Plus, he had the added challenge of a relatively low income. But with a little work, he was able to pay his big debt in a small amount of time.

“I was only making $30,000 a year,” said Eleazer. “My rent was $900 a month, and my loan payments were $1,200. But I was only making $2,500, leaving me with about $400 for everything else.”

It was then that Eleazer got serious about paying off the debt. Although his annual salary was only $30,000, he was able to pay off his debt in only two and a half years.

How to pay off $60k in student loans, even with a low salary

1. Do a cost-benefit analysis

Eleazer’s get-out-of-debt plan started before he even incurred $60,000 in student loans. He went to a state school for his undergrad education to keep costs down, then analyzed his options for graduate school. He could pay $50,000 a year at Columbia University or $15,000 at SCI-Arc.

“For architecture, [the] salary is based on experience, and where you went to school doesn’t matter so much,” he said. “You aren’t going to get a big salary right out of school. So, I sat down and projected out my salary for the next 10 years next to my debt.”

His projections made the decision easier. “It was clear I couldn’t afford to go to Columbia,” he said, and advised “do[ing] the math before you make the student loan decision.”

Check out job-hunting websites to research average salaries for your desired profession and use our student loan payment calculator to determine what your monthly loan cost would be versus your income. This cost-benefit analysis can help you decide if the grad school you want to go to is worth it.

2. Get good at budgeting

For a couple of years, Eleazer wasn’t going out and having fun in Los Angeles like some of his peers.

“I was eating and living very frugally,” he said. “My apartment was cheap for L.A., I didn’t spend money on dinners out and [I] bought the cheapest version of my necessities.”

To make a solid budget, write down your necessary expenses, including rent, student loan payments, food and utilities. Then, examine your credit card bill and bank statements to see where else your money is going. Ask yourself: Where can you cut back? Can you cancel that cable subscription? Can you find a cheaper apartment? Can you cook at home more?

All these tweaks will add up to big savings, which means you’ll have more money to put toward your student loan debt.

“It hurt my social life living on an extreme budget,” said Eleazer. “But in the long run, I was ahead. I get to live a different lifestyle now being debt-free.”

3. Adopt the debt snowball method

Shortly after graduating, Eleazer got exposed to author Dave Ramsey and adopted the debt snowball method he popularized.

“He has easy-to-follow rules,” Eleazer said. “List your debts from smallest to highest, regardless of interest. You pay off your smallest first while paying the minimums on the others because it gives you a high. Then, use the money from the small payment and put it toward the next debt until everything is paid off.”

Let’s say you have student loans with balances of $5,000 and $10,000. Pay off the $5,000 loan first while paying the minimum monthly balance on the $10,000 one. Once you repay the smaller loan, use that monthly payment money to pay down the $10,000 debt. Keep following that pattern until you’re debt-free.

You also can look into the debt avalanche method, which focuses on the interest rates of the loans rather than the balance while paying down debt.

4. Take on a side hustle

If you aren’t making enough money, you need to figure out how to earn more.

“In addition to my job, I found side work,” he said. “Find ways to supplement your income. I worked nights and weekends teaching workshops at UCLA, worked for professors and spoke at seminars around the world to bring in extra cash.”

Eleazer was able to find side gigs that were in his line of work, but you can take on a variety of side hustles that don’t require a particular background. Become an Uber driver, deliver food for DoorDash or help someone with some handy work with TaskRabbit, to give a few examples.

5. Put any extra money toward debt

Bringing in extra income through your side hustle is only half the battle — you need to put that money toward your debt.

“I still always lived like I only had that $400 a month,” said Eleazer. “All of the money I made from my side hustle, which was about $10,000 to $15,000 a year, went toward paying my student loan debt. Then, I got a $4,000 gift from my grandmother and $2,000 from my now-wife. Every penny went to the debt.”

If you get a bonus, tax refund or birthday money from your mom, resist the urge to spend it on a new pair of shoes. Instead, pretend like you don’t have that extra income and put it immediately toward your loans. This effort will help you tackle your debt quickly.

Paying off your student loan debt fast

It can seem daunting to repay your student loans when you’re not making much money. But it can be done. Eleazer made sacrifices for a few years, but he now can live a life free of money concerns.

These tips could help you get out of debt without having to worry about bringing home the big bucks (of course, that would help, too). If you make more money, you should put it toward paying off your debt before using it for any other type of spending.

“My relationship to money has changed completely,” said Eleazer. “I still live by the philosophy to never stop working even when you pay the debt off.”

“It’s now a lifestyle choice,” he added. “I have fun, but spend money differently than other people do.”

70000 student loan monthly payment

The unconventional way this man paid off $70,000 in student loans

Published Thu, Apr 5 20183:34 PM EDTUpdated Thu, Apr 5 20183:34 PM EDTKat Tretina, Student Loan HeroSHAREShare Article via FacebookShare Article via TwitterShare Article via LinkedInShare Article via Email1:06This breakout lead used her ‘Star Wars’ salary to pay off student loans

When Ray Laureano and his wife graduated from college, they left school with a staggering amount of student loans. Between the two of them, they were over $200,000 in debt.

“We had a huge amount of student loans,” says Ray. “I started researching how to pay them off quicker so we could get out from this debt.”

After doing his homework, Ray came up with an unconventional approach to debt repayment. Although it goes against what most financial experts preach, it worked for him; Ray and his wife paid off over $70,000 in just one year.

Here’s how they did it and what you need to know before copying Ray’s strategy.

Getting into student loan debt

Ray works as a business analyst and helps companies improve their performance — a field that requires advanced degrees. Both he and his wife went to private colleges rather than public universities, which significantly added to their college costs. However, they saved money where they could.

“I enrolled in an accelerated program [at Robert Morris University-Illinois],” he says. “I did a dual degree, earning a bachelor’s and two master’s degrees in four years.”

Although his unique program was cheaper than it would have been to earn each degree individually, his education costs still added up quickly.

But Ray took on the debt with his eyes wide open. “I knew a ballpark estimate of what to expect for my starting salary in the technology field,” he says. “I knew what I was getting into.”

The parents of both Ray and his wife had also taken out Parent PLUS Loans to help them pay for school, but the couple felt responsible for that debt.

Ray LaureanoSource: Student Loan Hero

“To me, I felt we morally needed to get them out of debt,” Ray says. “It’s our responsibility, in my mind. We didn’t want to hold our younger siblings back [from going to college] because our parents had to worry about those loans.”

By the time Ray and his wife graduated, their loan balance was more than $200,000. Thankfully, they both relied on federal loans to pay for school, so they had lower interest rates than they would have had if they used private student loans. “Our interest rates ranged from 3.00 percent to 8.00 percent on our loans,” he says.

Coming up with a repayment plan

Ray started researching his repayment options and looked for a tool he could use to see all of his family’s loans at once. His search led him to Student Loan Hero’s app, which helped him get started.

The tool let him see all of the couple’s loan balances, interest rates, and monthly payments in one place. With a loan dashboard in place, the couple became focused on paying off their debt as soon as possible. They used the debt avalanche repayment method, where you target the highest-interest debt first.1:21This couple is trying to pay off $600,000 of student loans in 5 years

Ray and his wife have a combined income of $110,000. Although that sounds high, payments on $200,000 in student loans eats up a significant portion of their pay.

To help free up extra money to put toward their loans, the couple lives on a strict budget. That approach allows them to put more than $4,500 per month toward their debt on top of their regular payments.

“We’re being very intentional with our money,” Ray says. “We do a lot of preplanning. If it’s not in the budget, we just don’t spend the money.”

A radical debt repayment strategy

Besides cutting their expenses and sticking to a budget, Ray and his wife decided on a nontraditional plan for debt repayment.

Conventional financial advice says that if you follow the debt avalanche repayment strategy, you make the minimum payments on all of your debt and put any extra money toward the debt with the highest interest rate.

For Ray, that approach didn’t seem effective enough. Instead, he talked to each loan servicer and entered the lower-interest loans into forbearance; in other words, he paused payments on those loans.1:13Here’s where students have the hardest and easiest time paying off loans

With his other debt payments on hold, he put all of his extra money toward just one loan with the highest interest rate. When that loan was fully paid off, he tackled the next highest-interest debt, and so on.

It’s a radical approach that’s not for everyone. When you enter your loans into forbearance or deferment, interest continues to accrue on those loans, so you can end up paying more in interest fees over the length of your loan. But for Ray, seeing the progress they made on each loan was highly motivating.

“Having a high intensity focus on one loan at a time — the highest-interest one — kept us moving forward,” he says.

Next steps for paying back his loans

With this strategy in place, Ray and his wife managed to pay off $70,000 in student loans in just one year. If they maintain this pace, Ray estimates that they will be debt-free by March 2020.

For others who find themselves overwhelmed with debt, Ray advises borrowers to start tracking your expenses and income.

“Many times, people let the huge amount of debt blind them and they get paralyzed by their student loan balance,” he says. “Really, just get on a budget — that’s what is going to get you through.”

As Ray’s experience shows, there’s no one way to pay off your debt. You need to pick a debt repayment strategy that works for you in the long term. Even if your approach is unconventional, if it keeps you motivated and on track to pay off your debt, it might be the perfect plan for you.

If you want to pay off your loans ahead of schedule, check out our ultimate guide to paying off your loans faster.

student loan payments

Make a Student Loan Payment

It’s simple to pay toward your student loan—at any time. Get started by working with your federal loan servicer.

Where to Send Payments

Your student loan servicer handles all billing regarding your student loan. Your servicer can work with you if you need help to make a payment.

Make a Payment to Great Lakes and Nelnet

We are now accepting payments for federally-owned student loans serviced by Great Lakes or Nelnet!* Visit your account dashboard to find out.

Make a Payment to Great Lakes or Nelnet

*If we aren’t able to accept your payment due to your account status, or if you prefer to pay on your servicer’s website, log in to your Great Lakes or Nelnet account.

Make a Payment to Other Loan Servicers

Direct Loans and Federal Family Education Loan Program loans owned by the U.S. Department of Education (ED)

- FedLoan Servicing (PHEAA)

- Great Lakes Educational Loan Services, Inc.

- HESC/Edfinancial

- MOHELA

- Aidvantage

- Nelnet

- OSLA Servicing

- ED Held Perkins Loans / ECSI

- Default Resolution Group (also known as Maximus Federal Services, Inc.)

- Not sure who your loan servicer is? Visit your account dashboard to view your loans and make a payment.

Federal Family Education Loan Program loans not owned by ED

- The bank, credit union, or other lending institution that made the loan (also known as “the lender”)

Federal Perkins Loans

- Your school or the billing agency your school designates

Never miss a payment. Sign up for automatic debit through your federal loan servicer to have your payments automatically taken from your bank account.

Bonus! If you have Direct Loans, get a 0.25% interest rate deduction while you participate in automatic debit!

student loan amortization schedule

6 Things to Know About Student Loan Amortization

Understanding this concept can help borrowers avoid inadvertently increasing their total student loan balance.

Understanding Student Loan Amortization

You will continue paying the same amount monthly on your student loan, but the portion that is applied to interest changes over the life of the loan. (GETTY IMAGES)

Making a financial plan to repay your college student loans can be overwhelming, but it doesn’t have to be. Amortization is one of many technical terms that may seem like an intimidating concept, but understanding it is key to finding the right repayment plan and paying off your student loan faster.

Here are six things you need to know to understand student loan amortization:

- The vast majority of student loans are installment loans.

- All student loans are amortized.

- Amortization changes over time.

- An amortization schedule can show you how your payments are being applied.

- Your repayment plan affects your amortization schedule.

- Negative amortization can make your loan balance grow.

The Vast Majority of Student Loans Are Installment Loans

There are generally two types of loans, revolving and installment.

Revolving loans, like your credit card, provide a line of credit from which you can borrow continuously. Installment loans are borrowed in a lump sum and paid back over time on a payment schedule. All federal student loans and most private student loans are installment loans.

You may have borrowed at the start of each school year to pay tuition and other education-related expenses, but that likely just means that each year you took out a new student loan. Unless you consolidate or refinance, each of your student loans is a separate installment loan.

All Student Loans Are Amortized

All installment loans, which include student loans, are amortized. Amortization is the process of paying back an installment loan through regular payments.

When a student loan is amortized, that means that a portion of the monthly payment is applied to interest and a portion is applied to reduce the principal balance.

Amortization Changes Over Time

Although you will pay the same amount every month on your student loan, the portion of your payment that is applied to interest changes over the life of the loan.[

In the beginning, most of your payment is applied to interest. Even though you are making regular payments each month, the principal loan balance decreases more slowly during this period.

Don’t worry, though! As your principal balance declines, less interest accrues each month, so more of your monthly payment is applied to the principal, reducing your student loan balance more quickly.

If you can pay more than your fixed monthly payment, you can pay your student loan off faster and lower your total payments by requesting that any additional amount be applied to the principal. Just make sure to talk with your student loan servicer about how to apply the payments. Your servicer is the organization that sends you bills and collects your payments.

An Amortization Schedule Can Show You How Your Payments Are Being Applied

An amortization schedule is a table that shows the amount of principal and interest that you pay each month over the life of a loan. While each payment that you make is the same amount, remember that the amount of interest paid by each payment decreases over time.

To better understand how this works and to see how your payments are being applied, request an amortization schedule from your loan servicer.

Your Repayment Plan Affects Your Amortization Schedule

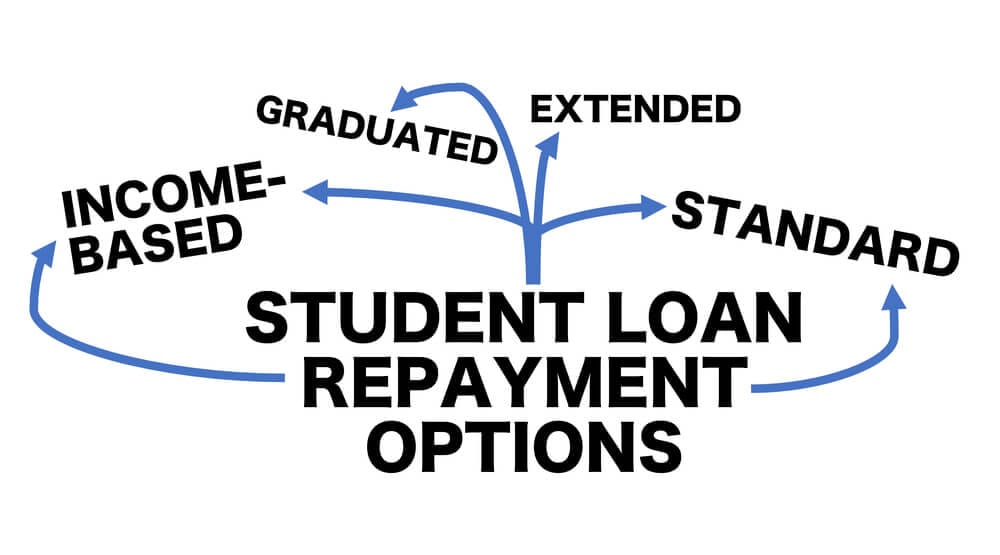

If you have federal student loans, you can select from several different repayment plans that affect how quickly you will repay each loan. Standard repayment – in which payments are fixed and made for up to 10 years – is the fastest way to repay your loan, because you will pay more each month over a shorter period of time.[

READ: What to Know About Federal Student Loan Repayment Options. ]

However, if you have trouble managing the monthly payments under the standard repayment plan, you might consider enrolling in a graduated repayment plan, which starts with lower monthly payments that increase every two years, or applying for an income-driven repayment plan, which sets monthly payments based on your income and family size.

These changes will affect your amortization schedule, and you should talk to your loan servicer to better understand the impact.

For private student loans, check with your lender about the terms and conditions related to repayment.

Negative Amortization Can Make Your Student Loan Balance Grow

Be careful! If your monthly payments are lower than the amount of interest that accrues, the unpaid interest may capitalize and become part of the principal. This is called negative amortization.

Negative amortization can make the total amount that you owe on your student loan increase over time – even while you are making monthly payments. If possible, always try to pay the full amount of interest that you owe each month, and asking your servicer for an amortization schedule can help you do that.

As your situation changes, you may consider moving into a repayment plan with a higher monthly payment so that the payments will decrease your principal balance faster over time. Your servicer can help you understand those options.

By understanding how amortization works, you can make better financial decisions as you work to reduce and eventually pay off your student debt.

Leave a Reply