In this guide, we review the aspects of: are student loans simple or compound interest, how are student loans compounded, how often are student loans compounded, do student loans compound daily, and are student loans compounded monthly.

If you have student loans, you may be wondering whether they’re simple or compound interest. The answer may surprise you! In this guide, we review the aspects of: are student loans simple or compound interest, how are student loans compounded, how often are student loans compounded, do student loans compound daily, and are student loans compounded monthly.

Are Loans Simple Or Compound Interest

When you take out a student loan, the lender will charge you interest on your outstanding balance. The amount of interest charged is determined by the type of student loan and how much you owe.

The amount of interest charged varies depending on whether you have a fixed rate or variable rate student loan. It also depends on whether your loan has been consolidated with other loans or not.

There are two types of student loans: direct subsidized and unsubsidized (also known as subsidized and unsubsidized). Direct subsidized loans are those which have been paid off by the US Department of Education. Unsubsidized loans are those which have not been paid off by the US Department of Education. These include both Stafford and Perkins loans, among others.

One of the first things you learn when it comes to money management is the concept of interest, which comes into play when you’re lending or borrowing money. Lenders earn interest on the money they lend, while the borrowers pay interest on the money they borrow. Interest is a percentage of the money you borrow or lend that is paid periodically. Although it’s typically quoted on a yearly basis, interest can last for as long or as short a time as the lender requires.

It’s important for borrowers to note that when they pay back the money they borrowed, they typically pay interest. For example, think of a credit card with an annual percentage rate (APR) of 1 percent; when you pay off your bill, you pay the amount you owe in addition to the 1 percent interest. This means you end up paying more than you borrowed.

However, it’s important to remember that interest is typically introduced as simple interest when there are actually two types of interest: simple vs. compound interest. Compound interest is when the amount of interest you pay increases in an upward curve, similar to a snowball effect. Keep reading to learn about the difference between the two and how they apply to your finances.

What Is Simple Interest?

Interest is a fee you pay on top of the money you borrowed when you pay it back, and simple interest is the most basic type of interest you pay. The rate of simple interest doesn’t increase over time so you’ll always know how much you’ll pay.

For example, if you have a credit card with 5 percent APR on which you bought $1,000 worth of purchases, you would ultimately pay back the $1,000 borrowed from the credit card company in addition to 5 percent interest on $1,000 — paying off your entire balance including the simple interest would cost $1,050. Keep reading to learn how to calculate simple interest.

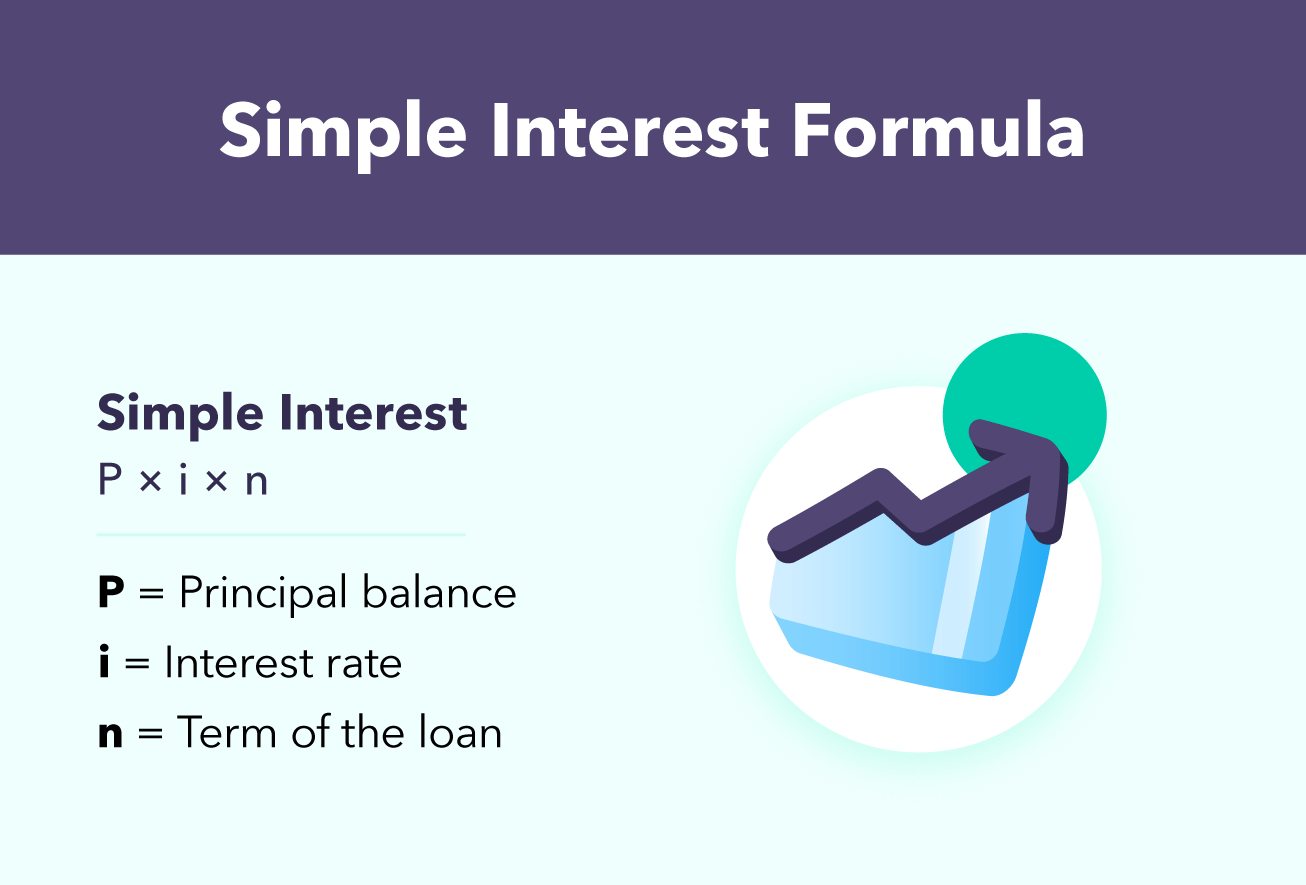

How to Calculate Simple Interest

Similar to the scenario above, calculating simple interest involves three elements: the principal balance, interest rate, and term of the loan. The principal balance is the amount of money borrowed or lent, the interest rate is the additional fee and the term of the loan is how long the money is borrowed or lent before repayment. Check out the simple interest formula below.

Simple interest = principal balance x interest rate x term of the loan

What Is Compound Interest?

Compound interest is a fee on a loan or deposit that accounts for the principal balance in addition to the interest accumulated from previous periods.

You may hear compound interest referred to as paying interest on interest. Another factor that influences the interest rate is the frequency of compounding. In other words, the greater the number of compounding periods, the greater the interest rate will be.

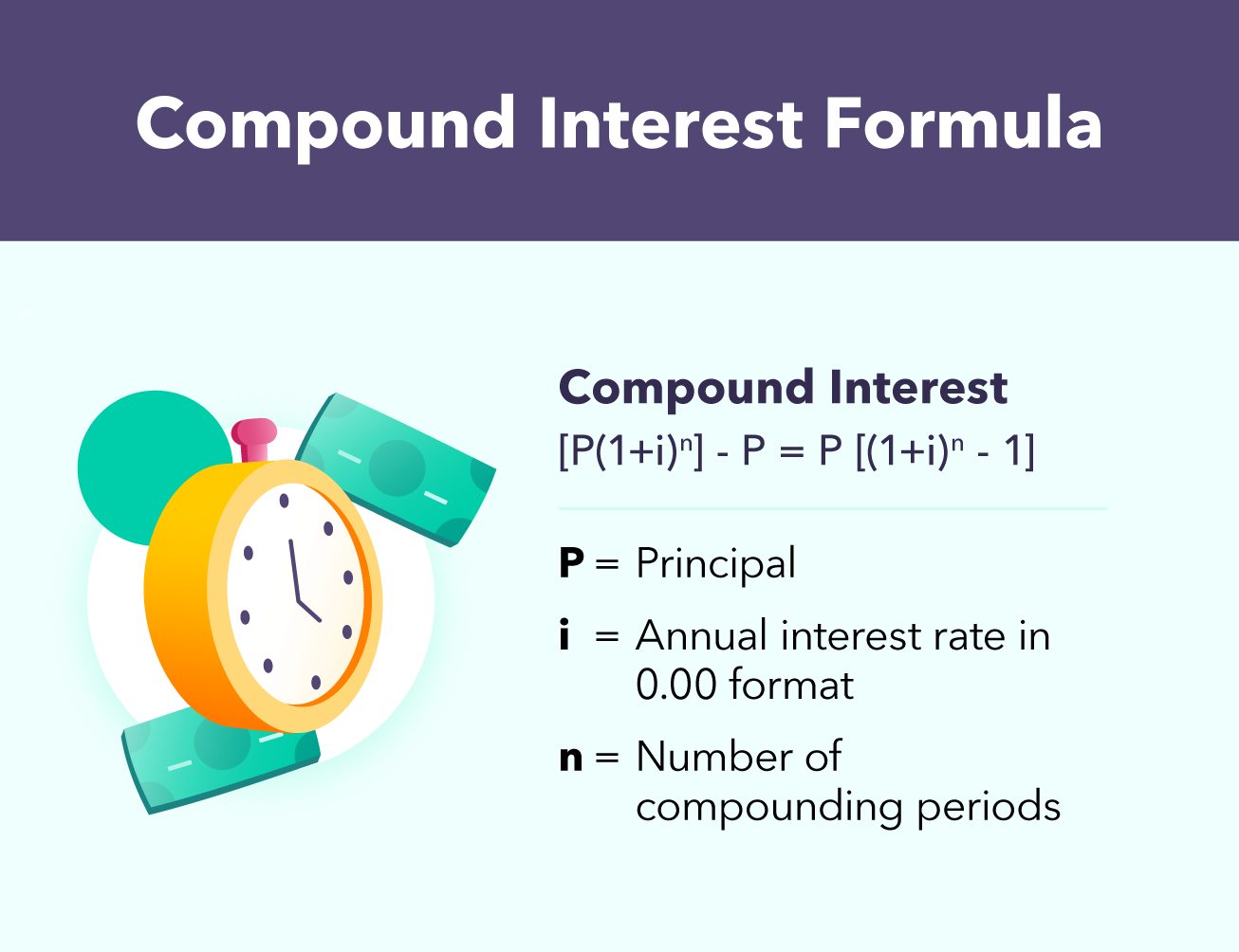

How to Calculate Compound Interest

Calculating compound interest involves multiplying the principal balance by one, and then adding the annual interest rate raised to the number of compounding periods minus one. Consequently, the total principal balance is subtracted from the value of the compound interest equation. Find the compound interest formula below.

To easily calculate compound interest, check out our compound interest calculator.

Difference Between Simple and Compound Interest

What differentiates simple versus compound interest is that the latter will make the amount owed grow at a much faster rate than simple interest. This is because simple interest is calculated based only on the principal balance, whereas compound interest is calculated based on the principal balance and the accumulated interest from the previous periods.

Compounding periods are the key element that differentiates simple and compound interest. This is why there is a significant difference in how much interest accrues in instances of compound interest. The greater the number of compounding periods, the greater the amount of compound interest owed.

Real Life Applications

Here’s where we apply what we’ve learned to your finances. Simple interest is typically used when obtaining credit card loans, car loans, student loans, consumer loans, and sometimes even mortgages.

On the other hand, compound interest is often used to boost investment returns in the long term, like 401(k)s and other investments. Another common use of compounding interest is in bank accounts, particularly savings accounts. Student loans, mortgages, and credit cards can also use compound interest so be sure to keep an eye out for the interest rate when making big financial decisions like these. There are no hard and fast rules for what purchases constitute simple or compound interest, so be sure to ask your lender or do your research before borrowing money.

Understanding simple and compound interest is valuable in helping you take control of your finances. Whenever you’re borrowing money, it’s highly likely that interest rates are involved. This makes it even more important to understand the ins and outs of interest and how to maximize your money management. Whether you’re looking to take out a car loan, pick the best credit card, or simply looking to better understand how interest rates work, you’re already off to a great start!

are student loans simple or compound interest

We begin with are student loans simple or compound interest, then how are student loans compounded, how often are student loans compounded, do student loans compound daily, and are student loans compounded monthly.

Student loans are a big, scary thing. You’ve probably heard that student loan debt is the number one cause of bankruptcy in America, but you might be wondering what exactly that means for you.

Well, there are two main types of interest rates: simple interest and compound interest. With simple interest, you pay interest only on your principal amount and don’t accrue interest on your unpaid interest. This means that if you have a $100 loan at 10% annual simple interest, by the end of year one, you’ll owe $110—$10 in principal plus $10 in interest for a total of $120. At the end of year two, your total balance is still just $120 because there was no new interest added to it over time—just the same old 10% annual rate applied to whatever was left unpaid from year one (in this case: $98).

With compound interest, however, each year’s unpaid principal amount grows larger and larger as it accrues more and more interest each time around until eventually it’s so big that it’s either paid off or something else happens to bring down its growth rate (like repaying some of it).

how are student loans compounded

Next, we review how are student loans compounded, how often are student loans compounded, do student loans compound daily, and are student loans compounded monthly.

Student loans are compounded interest. This means that if you don’t pay your loan on time, each day’s interest is added to your principal balance. For example, if your loan balance is $30,000 and your initial daily interest amount is $3, the next day that interest is added to the principal, so you’ll be charged interest on a total of $30,003.

This means that if you don’t make any payments at all for 30 days and then make one payment of $1,000 at the end of those 30 days, you will have actually paid back $31,000!

how often are student loans compounded

More details coming up on how often are student loans compounded, do student loans compound daily, and are student loans compounded monthly.

It’s important to understand how student loans compound. Even though student loan rates are expressed as an annual rate, the interest is usually compounded daily. On a $10,000 loan, you might think that a 4.45% interest rate would mean $445 paid in interest during the year, but that’s not the case. Instead, your annual rate is divided by 365, to get your daily interest rate.

The reason for this is pretty simple: if you were to pay off your entire loan at once, you’d only be charged one payment of interest. But if you have monthly payments, or if you make only partial payments throughout the year (which many borrowers do), then each time you pay off some of your debt, you’ll still be charged interest on what is left over—which means that over time, the amount of interest that builds up on your loan can add up quickly!

do student loans compound daily

Student loans accrue interest daily, and in most cases, interest doesn’t compound daily.

There are two types of student loan payment periods:

- The standard repayment schedule, which is 10 years for federal student loans and 12 years for private student loans. This means that each month, you’ll make a fixed monthly payment that covers the accrued interest and at least a portion of the principal balance.

- Income-driven repayment plans (IDR) can extend your loan term to 20 or 25 years if you have a high amount of debt relative to your income (or vice versa). IDR plans also cap your monthly payments based on your income and family size; this could mean that you’re only paying off interest each month with no principal reduction.

are student loans compounded monthly

So, you’re thinking about borrowing money for college. And you’re wondering how much that loan is going to cost you.

Well, we can help! We’ve got some answers for you on student loans and how they work.

First things first: even though student loan rates are expressed as an annual rate, the interest is usually compounded daily. What this means is that every day that passes, your total balance will increase by 1% of your original loan amount. So if you borrow $100,000 at 5%, you’ll owe $5,000 in interest after a year—but if you choose to pay it back over 10 years instead of 15 (like most people do), then each month will see an extra $500 added to your principal balance.

How Does Student Loan Interest Work?

For undergraduates, the student loan interest rate for Direct Unsubsidized and Subsidized loans is now 4.99%, and the rates are higher if you’re pursuing a graduate degree.

Understanding student loan interest is crucial to avoid taking on too much debt and to pay down what you owe.

This guide will show you how student loan interest is calculated, the different interest rates available, and provide tips to get the lowest possible rate on your loans.

How does student loan interest work?

Student loan interest rates are based on three main factors:

- The amount borrowed

- The type of loan

- The estimated time it takes to repay

Interest rates vary by lender, so borrowers should shop around and compare rates before taking out a loan.

You’ll get your interest rate when you apply for a federal or private student loan. This rate is the annual percentage rate (APR), which is the actual yearly cost, including interest and fees (but not compounding) for the loan term.

Federal student loans have fixed interest rates which Congress sets. Private student loans can have either a fixed or variable APR, and your lender determines your rate.

Check out the main differences in the table below:

| Fixed rate | Variable rate |

| Remains the same for the life of the loan. | Changes with its underlying market index. |

| Makes budgeting for payments easy. | Could rise or fall based on market rates. |

| Can change as often as every month, but typically changes every 6 – 12 months. |

Depending on whether interest accrues daily or monthly, the interest your loan generates is tacked onto your total balance each day or month.

The balance includes the principal (initial borrowed amount) and interest accrued. You must repay the interest before paying down the principal balance, so not paying makes your debt more expensive over time.

How do interest rates differ between federal and private student loans?

Interest rates are often lower on federal student loans than private student loans. Federal student loan interest rates are fixed for the whole loan period and may not exceed the maximum rates listed in the Higher Education Act of 1965:

- 8.25% – Direct Subsidized Loans and Direct Unsubsidized Loans for undergraduates

- 9.50% – Direct Unsubsidized Loans for graduate or professional students

- 10.50% – Direct Parent PLUS loans

These are the maximum allowed rates for federal student loans, but often the rates are much lower. For example, federal student loan interest rates range from 4.99% to 7.54% for 2023.

Loans from private student lenders have no maximum limit, and variable interest rates can balloon to be much larger than the initial interest rate of your loan. In 2022, private student loan rates varied from 3.99% to 15.66%.

It may seem best to choose the loan with the lowest interest rate, but also consider the other terms of the loan. Variable interest rates may start out lower than fixed rates but are subject to change, which could increase your monthly payment.

More flexible repayment options are available for federal student loans, including income-based repayment plans and deferment. These options are not available for many private loans.

How often does student loan interest compound?

Compound interest is the addition of interest to the principal of a loan—interest on the interest. Most student loans accrue interest daily and compound daily or monthly.

Daily compounding means your APR applies to the interest that accrued the previous day. This is in addition to the rest of your principal amount.

Compared to monthly, daily compounded interest is less advantageous for you because the more often your interest compounds, the faster your debt will grow.

In most cases, student loan rates are advertised with yearly interest rates (APR), but the interest compounds daily. You can find out how often your interest accrues as well as your compounding rate on the promissory note for your student loans.

How to calculate student loan interest

Using the simple daily interest formula, you can calculate your interest the following way.

Begin by determining your interest rate factor using the following calculation:

Fixed interest rate of your loan / Number of days in a year = Interest rate factor

Then multiply the following:

Principal balance x Interest rate factor

Let’s assume you take out a $10,000 student loan with a 5% APR.

The interest rate factor is 0.0137% (0.05 / 365 = 0.000137).

Here’s what your interest would look like with daily compounding compared to monthly compounding:

| Daily compounding | Principal x Interest rate factor | Total principal + interest |

| Day 1 | $10,000 x 0.000137 | $10,001.37 |

| Day 2 | $10,001.37 x 0.000137 | $10,002.74 |

| Day 30 | $10,039.81 x 0.000137 | $10,041.18 |

In this example, $41.18 of interest has accrued in a month.

| Monthly compounding | |

| Principal x Interest rate factor x Number of days | Total principal + interest |

| $10,000 x 0.000137 x 30 | $10,041.10 |

Over a month, $41.10 of interest has accrued.

As you can see, daily compounding results in slightly higher interest charges over a month.

The difference will be insignificant if you make monthly payments that cover all the interest that has accrued that month.

But if you don’t keep up with your payments, the interest that accrues each day will continue to grow as the daily interest adds to your principal balance. It’s important to meet your repayment obligations on time and in full each month because it will help minimize your total debt burden over the long term.

When does student loan interest start accruing?

You will start accruing interest at different times depending on the type of loan you take out.

In some cases, interest begins accruing upon disbursement. This is always the case with private student loans and federal Direct Unsubsidized Loans. If you don’t make interest payments while in school, the interest will accrue throughout your years in college.

In the case of federal Direct Subsidized Loans, the federal government covers your accrued interest while you are in school and over a six-month grace period after you graduate. Once those six months are up, you are responsible for repaying the principal and the interest.

| Type of loan | Borrower type | Fixed interest rate (as of January 2023) | Start of interest accrual |

| Direct Subsidized Loans | Undergraduate | 4.99% | 6 months after graduation as long as you are enrolled at least half-time |

| Direct Unsubsidized Loans | Undergraduate | 4.99% | Upon loan disbursement |

| Direct Unsubsidized Loans | Graduate or Professional | 6.54% | Upon loan disbursement |

| Direct PLUS Loans | Parents and Graduate or Professional Students | 7.54% | Upon loan disbursement |

Federal student loans

You don’t have to start paying student loan interest right away

Even for most unsubsidized loans, such as those from private lenders, you won’t have to start paying interest immediately. Many private companies allow for a grace period, which can be excellent news for students who can’t take on a job during college.

Under certain circumstances of financial hardship, such as a period of unemployment or reduced income, borrowers can work with their lenders to enter deferment or forbearance and temporarily freeze or decrease their monthly payments.

This action helps the borrower avoid default when money gets tight.

| Forbearance | Deferment | |

| Definition | Loan repayment relief that allows you to temporarily reduce or freeze payments on student loans if you are experiencing a financial hardship. | Temporary suspension or reduction of your monthly loan payments. |

| Difference | Interest continues to accrue and is added to your principal balance when your forbearance ends. | You will not have to make any principal payments on your loans. However, you must pay interest on Direct Unsubsidized, Direct PLUS, Federal Family Education Loan (FFEL) PLUS, the unsubsidized portion of Direct Consolidation, and the unsubsidized portion of FFEL Consolidation loans |

Regardless of these options for postponement, keep this in mind: Once you receive an unsubsidized loan, if you forgo payments through the six-month grace period after you leave school, you might already owe thousands more than you borrowed.

In this case, it will take several payments before you begin paying down the principal.

How to pay off the interest on student loans faster

The faster you pay off your student loan interest, the faster you can start paying off your principal balance, which will reduce your interest over time.

If you’re tired of paying interest on your loans, here are the steps to paying off your loans early.

Prioritize your loans

One way to pay off your student loans faster is to prioritize your loans by interest rate.

Once you’ve established your payment schedule with automatic payments of at least the minimum required amount, allocate any remaining resources to the loan with the highest rate.

You can see an example of this in table below:

| Example prioritization | |||

| Payoff order | Loan | Balance | Interest rate |

| 1 | Loan B | $10,000 | 7.80% |

| 2 | Loan C | $3,000 | 6.50% |

| 3 | Loan A | $5,000 | 4.99% |

Make extra payments

We recommend making extra payments whenever possible—especially if your interest compounds daily. A second monthly payment helps minimize the amount of time interest can accrue while you pay down the principal.

A smart way to handle this is to make a payment every time you get paid (if you get paid every two weeks). Your first paycheck can cover the interest you’ve accrued in the previous month, and the second will eat away at the principal and limit the interest that accrues in the subsequent month.

For example, if you were paying off a $10,000 loan at 7.8%, you’d have a monthly payment of about $120.

If you made two payments each month of $120, you would pay off your loan in four years instead of 10 and save $2,700 on interest:

| Current | 2 payments per month | Savings | |

| Repayment length | 10 years | 4 years | 6 years |

| Interest payments | $4,433 | $1,700 | $2,731 |

| Total cost | $14,433 | $11,700 | $2,731 |

Calculate how an extra payment could save money on your student loans with our student loan prepayment calculator.

Refinance

Refinancing student loans is another smart way to abate the pileup of interest. If you think you might qualify, apply for a loan with lower interest rates from a private company, or check whether you can refinance through a state-run program.

Be aware that refinancing federal student loans with a private lender will forfeit any borrower protections you get with federal loans, such as eligibility for income-driven repayment or the potential for student loan forgiveness.

Take a look at how refinancing a $10,000 student loan with an 8% interest rate to a loan with a 5% interest rate could lower your monthly payments by just $15 but save you more than $1,800 over the life of the loan:

| Current | Refinance | Savings | |

| Monthly payment | $121 | $106 | $15 per month |

| Term length | 10 years | 10 years | 0 months |

| Total interest | $4,559 | $2,728 | $1,831 |

| Total cost | $14,559 | $12,728 | $1,831 |

Calculate how refinancing your student loans could save you money with our student loan refinance calculator.

How can I lower my student loan interest rate?

Our additional tips for lowering student loan interest rates are as follows:

- Refinance: If you have good credit and a steady income, you can refinance your student loans with a private lender or through your state at a lower interest rate.

- Consolidate: Consolidate federal student loans into one monthly payment through the Department of Education’s Direct Loan Consolidation program.

- Autopay discounts: Many loan servicers reward borrowers for setting up automatic payment plans. Check with your lender to see what discounts are available.

- Get a cosigner: Having a parent or significant other with a high credit score attached to your loan can give a private lender peace of mind the money is in good hands, helping you qualify for a lower rate. Or if you have good credit but don’t make enough money to qualify for a lower interest rate, you can get a loan or refinance your loan with a cosigner who qualifies.

- Improve your credit score: Making on-time payments each month can help you improve your credit score and increase your odds of qualifying for a lower interest rate for new or refinanced loans.

These options offer a greater chance of paying down your student loan interest and then the principal sooner.

Do your best to keep on schedule, get ahead when you can with additional payments, and remain aware of what you owe.

If you need any more support in deciding how best to navigate your student loan situation, check out our in-depth guide on how to save money on student loans.

Leave a Reply