To get all the important details you need on Can I Take Out a Student Loan for Living Expenses, What can student loans be used for, How to Use Student Loans for Living Expenses and lots more All you have to do is to please keep on reading this post from college learners. Always ensure you come back for all the latest information that you need with zero stress.

Hi! Welcome to the world of student loans, where you can live like a king (or queen). You might be thinking: “I have no idea how I’m going to pay for my education.” But don’t worry! We’re here to help.

First of all, remember that student loans are designed to help you pay for your education by giving you access to money when you need it most—when it’s too late for scholarships or grants. They’re not just for tuition, either: they can also be used for books, housing, and other expenses related to going to school.

Another thing that’s important is that you understand how much your loan will cost over time. Student loans are usually paid back over 10 years, but if you take out a loan with a higher interest rate than 3%, it could end up costing more than what you borrowed in the first place!

We recommend looking into both federal and private options before choosing one specific lender or type of financing because there are many different types of student loans out there—and each one has its own set of benefits, drawbacks, eligibility requirements and repayment options—so pick wisely!

is it illegal to spend student loan money

Is It Legal to Invest My Student Loan Money?

Student loans are distributed for the purpose of covering educational costs for attending college, and they come from both government and private lending organizations. In some cases, students who find themselves with excess money during college choose to invest student loans rather than returning them to the government. While this type of investment is not strictly illegal, it raises numerous ethical issues that result in a legal and moral gray area for aspiring student investors.

Between 1998 and 2000, a college student and inexperienced investor Chris Sacca used his student loans to generate an investment portfolio of more than $12 million, according to Inc.com. Sacca is an extreme example of the growing trend of college students who choose to divert money intended for educational expenses and attempt to generate a return in the stock market. Such a move is risky, but it’s not without its benefits, as wise investments can generate revenue that exceeds the interest on private and federal loans.

KEY TAKEAWAYS

- Investing student loan money is not illegal.

- However, such investing does fall in a legal and moral gray area.

- Borrowers of government-subsidized loans could face legal action if they invest the money, which may include repaying subsidized interest.

- Private student loans have fewer restrictions and students likely won’t face any recourse for investing that money.

- A bigger risk, however, might be the inability to generate sufficient return before repayment is due after graduation.

Investing Federal Government Student Loans

The biggest legal consideration when investing student loans is whether the loans are from a private lender or a U.S. Department of Education contracted lender. The Department of Education generally has more strict rules about accepted uses of student loan funds, while private lenders often trade higher interest rates for fewer restrictions.

One of the biggest differences between federal student loans and private loans is that the government subsidizes interest on some student loans as an investment in an educated population. Students who spend their federal loan money on noneducational expenses may not be breaking the law, but they could face legal action from the DOE if their actions are discovered. In some cases, this may include repaying subsidized interest.https://575bca9d3f2c1e745bcabc081f9699e9.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

Student Loan Amounts

The amount of student loans each student receives is based on a relatively complex formula that takes into account dependent status, parental income, yearly income, residency status and whether the student will be attending full- or part-time. The final figure is known as the cost of attendance, and it generally includes a living allowance for students who are living off-campus.

The living allowance is where the gray area of student loan use begins, as some students choose to invest student loans in excess of attendance costs in the same way that others choose to use them for unrelated living expenses. In cases where institutional scholarships cover the cost of tuition and room and board, students may find themselves with thousands of dollars in unused student loan money to return or invest.

Students who wish to invest student loans while incurring as little risk of legal action as possible should avoid investing government-subsidized loans. Investing the full amount of refunded student loans is also a risky move, and more conservative investors choose to stick to the excess amount allotted for general living expenses. While litigation is a possible risk, the real risk most student loan investors face is not being able to make a return on their investment before payments come due after graduation

Can I Take Out a Student Loan for Living Expenses

It’s obvious that you can borrow student loan money to cover the cost of tuition, but you may be wondering if you can also use some of that money to pay for living expenses. Good news: The answer is yes.

Cost of Attendance

Every school has a defined cost of attendance, which includes not only tuition and student activity fees, but also several other categories of expenses:

- Housing: the cost of room and board (if you live on campus) or an allowance for rent payments and food if you reside off campus;

- Textbooks and supplies: the cost of books and necessary supplies such as a computer;

- Transportation: the cost of commuting to school every day, or flying home for the holidays if you attend school far away;

- Loan fees: upfront fees (if any) assessed by the lender at the time of loan disbursement;

- Dependent care: for students with children, the cost of providing day care for dependents; and

- Study-abroad programs: costs associated with eligible study-abroad programs.

[How much should I budget for college? Read our guide here.]

How Student Loans are Disbursed

Student loan money is typically paid by the lender directly to your school. The school keeps only enough money to cover the cost of tuition, and disburses the remainder directly to you. The amount you receive is known as your student loan refund. Your lender expects that you will spend this refund on education-related expenses, which may fall into any of the categories described above.

What Not to Do

Do not borrow more money than you actually need. Before applying for any student loans, prepare an estimated budget to determine the scope and scale of your likely expenses. If you are receiving financial support from family members, use that opportunity to borrow less. If you unexpectedly find yourself with extra loan money remaining at the end of the semester, consider repaying it immediately, or paying off other high-interest debt that you may have. Whatever you do, remember: Every dollar that you borrow must be paid back eventually – with interest!

How to Use Student Loans for Living Expenses

Student loans can be used to pay for college costs, including living expenses.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here’s how we make money.

Find the latest

- Ready for repayment? Forbearance ends Aug. 31

- Do you have a new servicer? Student loan servicer changes

- Will PSLF work for you now? Key forgiveness updates

- Keep your guard up: How to spot a student loan scam

Student loans are intended to pay for college, but education costs include more than tuition. You can also use student loans for living expenses.

You’re limited to borrowing the school’s cost of attendance — that’s tuition and fees, books and supplies, room and board, transportation, and personal expenses —minus any aid you receive.

» MORE: College survival guide for your money

Each college determines the cost of attendance, which covers expenses for one academic year and is adjusted yearly. Schools calculate numbers for on-campus, off-campus and commuter students, as well as for in-state and out-of-state tuition.

Both federal and private loans are disbursed directly to your school, which takes out tuition, fees and room and board if you live on campus. Any remaining funds from the loan will be distributed to you, according to your school’s policy. You may then return any funds you don’t need or use the money for living expenses, transportation, and books and supplies.

» MORE: When colleges say stay home: Options for all students

The following examples are compiled from guidance set by the Federal Student Aid office and private student loan lenders.

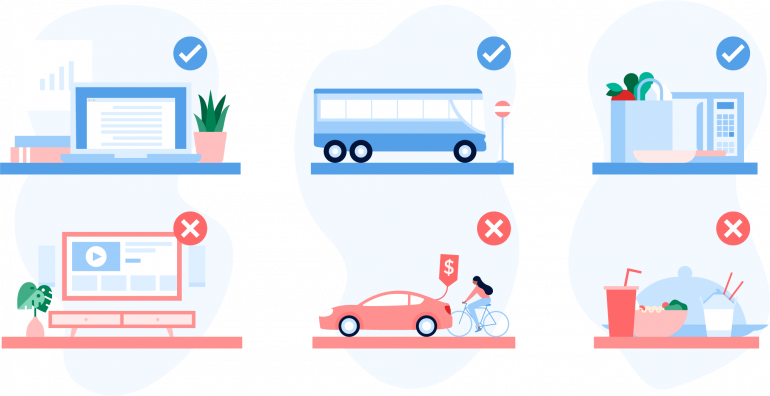

What can student loans be used for?

- Tuition and fees

- On-campus room and board

- Off-campus housing and utilities

- Transportation, including gas, tolls, buses and trains

- Books, supplies and equipment related to your major

- Miscellaneous personal supplies, including toiletries and medication

- Housing supplies, including linens, a microwave and dishes

- Groceries

- Care for dependents, as long as you let your school’s financial aid office know this allowance should be factored into your aid package

- Fees for professional testing, licensing and certificates

- Study abroad program costs

» MORE: Emergency financial aid for college students: What are your options?

What you shouldn’t use your student loans for

- Entertainment, such as concert tickets and Netflix subscriptions

- Pricey electronics, such as an oversized television or sound system

- Travel, vacations or hotel stays

- A new car, motorcycle or a bicycle

- Nightly takeout or delivery food

- A down payment or repairs on a home or car

- Small business expenses

- Other debt, such as personal loans, auto loans and credit cards

- Anyone else’s education costs

What happens if you use loan money for nonessentials?

Generally, no one is tracking how you spend your student loan money. But, you could face consequences if your lender finds out you misused student loan funds. Depending on your lender’s policy, your current loan and any future loan options may be terminated, and you could immediately owe the full balance of what you already used. The bigger deterrent to wasting borrowed money is that you have to pay it back — with interest.

Alternatives to using loans for living expenses

You can borrow to pay for living expenses, but that doesn’t mean you always should. You may be better off getting a part-time job while in school, tapping your savings or building up some cash by working during school breaks. This way you can pay for living expenses upfront without taking on more debt than you can afford.

Congratulations! You’ve made it through the first part of your life and are now a student. Now you have to learn how to live on student loans—and there are a lot of them.

Fortunately, there’s a lot of help available for you. Scholly is here to help you find scholarships, grants, and other financial aid so that you don’t have to take out as many loans or find yourself in debt after graduation. And if you do need some extra money in the meantime, consider working while going to school so that you can pay off your loans sooner.

If all else fails, know that there are many ways to get around paying back your student loans if you become disabled or face other hardships. You can also apply for deferment or forbearance if needed while waiting for those situations to resolve themselves. As long as you stay organized and keep up with any paperwork required by your lender or loan servicer, everything will work out just fine!

Leave a Reply