Student loans can be confusing as they often come with a myriad of acronyms, but they don’t have to be!. There are thousands of educational loans out there, so finding the best one can be overwhelming. First of all, before you take out any student loans, figure out if you can cover school expenses with scholarships, grants and education tax credits. Funding your education yourself will not only save you money but will also leave you debt-free after graduation. If that isn’t possible or if you’re feeling overwhelmed by the offers from the banks, this article is for you.

In this article, our focus shall be the US and we will be talking about; What Student loans should I get, Different student loans for different needs, How Student Loans Work and other related topics.

WHAT STUDENT LOANS SHOULD I GET?

1. Learn about different student loan types

Most students have two main options for student loans: federal (government) loans or private loans from banks, credit unions, and other lenders. You should research all your options for federal loans, also known as Direct loans, before shopping around for private loans.

The types of loans are:

- Direct Subsidized: A federal loan for undergraduate students. You don’t get charged interest while you’re in school. It is need-based, so whether you qualify depends on your FAFSA information.

- Direct Unsubsidized: A federal loan that any undergraduate or graduate student can get (as long as you haven’t reached your lifetime borrowing limit). You are charged interest while you are in school. To cut costs, pay the interest as you go.

- Direct PLUS: Federal loans for the parents of undergraduate students, or for graduate and professional students. You must pass a credit check to get these loans.

- Private: Loans offered by banks or credit unions. You should shop around for the best offer you can find. Students generally need a parent or other family member to co-sign.

Depending on where you live and other factors, you may have other options. Some states provide low-cost education loans for residents. There are also nonprofits and other organizations that offer low-or zero-interest student loans, often within a specific city or state.

2. Explore your federal options first

For most student borrowers, federal Direct loans are the better option. They almost always cost less and are easier to repay. (This may not be the case if you are a parent or graduate student considering federal PLUS loans, though.)

Here are some advantages of federal Direct loans:

- Access: Most students are eligible for federal student loans. There is no credit check (except for Parent PLUS loans). You will not need a co-signer, which private loans typically require.

-

Lower interest rates: For most borrowers, federal loans offer lower interest rates than private loans.

- If you qualify for subsidized loans, use them first. They are your cheapest option, since the government pays the interest while you’re in school.

- Fixed interest rates: Federal loans have fixed interest rates, meaning the interest rate will never change. Interest rates on private loan are often variable, which means your interest rates and payments could go up over time.

- Flexible repayment options: Federal borrowers have more options for reducing or pausing payments if they have trouble repaying their debt.

There are some downsides to federal student loans:

- If you default on your loan by not making any payments for 270 days, then the government can garnish (take) all of your tax refund and/or part of your wages or Social Security income.

- The amount of money you can borrow is limited. Freshmen can borrow up to $5,500; from your third year onward, the most you can borrow is $7,500.

Steps to getting a federal student loan

- Make sure your FAFSA form is complete and submitted.

- If you have selected a school, follow the instructions in the financial aid offer or ask the financial aid office. If you’re still applying to schools or waiting for, hang tight until you choose a school.

- Before you can get the loan money, you must complete entrance counseling and sign a Master Promissory Note.

3. If you still need a private loan, shop around to find the best deal

First, make sure you need a private student loan. We urge you to be cautious because private loans are generally more expensive than federal loans and offer little flexibility if you have trouble making payments later on. Your private loan interest rate and monthly payment could change with little warning, and you will have fewer options for when and how much you repay.

However, private loans may be a reasonable option for some borrowers, especially if you have strong credit history. Private lenders may allow you to borrow larger amounts, depending on your need and credit history. If you shop around and can show ability to repay, you may be able to find low interest rates relative to certain federal loans.

Steps to getting a private student loan:

- Talk to your school’s financial aid office. Most lenders require a form from the school certifying that you need additional aid to cover the cost of attendance.

- Line up a co-signer. Most private student loans require one unless the borrower has positive credit history. Co-signers are legally responsible for repaying the loan if the primary borrower doesn’t. You may want to consider loans that offer “co-signer release” after a certain number of on-time payments.

-

Shop around for lower interest rates and flexibility with repayment. Your credit score can take a hit from multiple credit applications, also known as “hard inquiries.” To reduce the impact, try to complete all applications within a 2-week period.

- Some private lenders advertise very low interest rates, which only borrowers with the best credit will qualify for. Your actual rate could be much higher.

- Don’t use a credit card. It can be a much more expensive way to finance your education. Credit cards do not provide the flexible repayment terms or borrower protections offered by federal student loans.

DIFFERENT STUDENT LOANS FOR DIFFERENT NEEDS

The average student loan debt among 2021 college graduates in the US who borrowed — 62% of all students — was $39,000.

Regional differences are significant. Higher-debt graduates emerge from colleges in the Northeast:

- New Hampshire, $39,410

- Pennsylvania, $39,027

- Connecticut, $38,546

- Rhode Island, $37,614

- Delaware, 37,447

- Maine, $33,591

- New Jersey, $33566

- Massachusetts, $33,256

Lower-debt graduates emerge primarily from colleges in the West

- Utah, $17,935

- New Mexico, $20,991

- Nevada, $21,254

- California, $21,485

- Wyoming, $23,444

- Hawaii, $23,557

- Florida, $24,629

- Washington, $24,645

With so many types of student loans for college, how do you pick the right one?

Even when narrowing your focus to federal student loan options, there are five different options with varying eligibility requirements, interest rates and maximum borrowing amounts.

To help you find your best option, here’s our overview of the six types of student loans available, depending on your needs.

1. FEDERAL STUDENT LOANS

There are several types of federal loans. The federal Direct Loan program is better known as Stafford Loans. These are available to undergraduate and graduate students alike. Money for these loans comes directly from the federal government.

Need-Based Loans or Subsidized Federal Loans

Students who cannot afford higher studies but have shown promise in academics are eligible for need-based loans. These loans are interest-free (while students are in school), and students get a limit within which they can borrow the amount. This limit may increase each year, meaning a student would be able to withdraw more money every year of their college than the previous one.

Also known as Subsidized Federal Loans, these are the most generous type of loans for a student to complete their higher education as they carry a low interest and are long-term.

Subsidized loans are reserved for students who can demonstrate a financial hardship. Most go to students whose families’ annual income is less than $50,000.

If you’re an undergraduate, the maximum annual amount of a subsidized loan depends on your year in school. Here’s the breakdown for students who are dependents (subsidized maximum in parentheses):

- First-year undergraduate, $5,500 ($3,500)

- Second-year undergraduate, $6,500 ($4,500)

- Third-year and beyond undergraduate, $7,500 ($5,500)

- Aggregate loan maximums, $31,000 ($23,000)

Here’s the breakdown for students who are independent (subsidized maximum in parentheses):

- First-year undergraduate, $9,500 ($3,500)

- Second-year undergraduate, $10,500 ($4,500)

- Third-year and beyond undergraduate, $12,500 ($5,500)

- Aggregate loan maximums, $57,500 ($23,000)

Federal Loan Benefits

As a federal loan borrower, you can take advantage of the following protections:

- Alternative payment plans: If you can’t afford your current monthly payments, you may be eligible for lower bills through an income-driven repayment (IDR) plan. Under an IDR plan, your payments will be based on your family size and income, and your repayment term will be extended to 20 or 25 years.

- Loan forgiveness: Some borrowers can have a portion of their loans forgiven through programs like Public Service Loan Forgiveness or Teacher Loan Forgiveness. You’ll also get forgiveness on any balance that remains at the end of your IDR plan.

- Deferment or forbearance options: In many cases, you can temporarily postpone making payments on your loans without becoming delinquent or entering into default—for longer periods than what many private lenders offer.

Federal Loan Limits

You can borrow PLUS loans in amounts up to the total cost of attendance at your school. Direct subsidized and unsubsidized loans, on the other hand, have annual loan limits. These loans depend on your year in school and whether you’re considered an independent student who won’t rely on family support.

| Loan Limits for Federal Direct Subsidized and Unsubsidized Loans | ||

|---|---|---|

| Dependent students | Independent students | |

| Annual limit for first-year undergraduate students | $5,500 (no more than $3,500 can be in subsidized loans, which the government pays the interest on in certain circumstances) | $9,500 (no more than $3,500 can be in subsidized loans) |

| Annual limit for second-year undergraduate students | $6,500 (no more than $4,500 can be in subsidized loans) | $10,500 (no more than $4,500 can be in subsidized loans) |

| Annual limit for third-year undergraduate students and beyond | $7,500 (no more than $5,500 can be in subsidized loans) | $12,500 (no more than $5,500 can be in subsidized loans) |

| Annual limit for graduate or professional degree students | All graduate and professional students are considered independent students | $20,500 (all unsubsidized) |

| Aggregate loan limit | $31,000 (No more than $23,000 may be subsidized) | $57,500 for undergraduate students (no more than $23,000 can be in subsidized loans), $138,500 for graduate or professional students (no more than $65,500 can be in subsidized loans) |

2. UNSUBSIDIZED FEDERAL LOANS

It is a long-term loan but is not on the basis of need. Under this, the interest is the responsibility of the borrower from the start of the loan. However, in some cases, one can postpone interest payments. .

Unlike subsidized federal loans, the unsubsidized version is also accessible to graduate and professional students, and awarding of the loan is not based on financial need or merit. In other words, almost everyone is eligible for this loan, as long as they’re enrolled at least half-time in school.

With unsubsidized loans, you’re on the hook for accruing interest while you’re enrolled, as well as during a grace period or while in deferment or forbearance. What’s more, the interest capitalizes when it goes unpaid, meaning that it will be added to the principal of the original loan amount.

Unsubsidized federal loans also carry a low interest and are best for a student who doesn’t qualify for other financial aid. Moreover, these loans are also helpful for those who need more funds to cover their financial expense.

3. Federal Plus Loans

Students attending the college in half or full-time undergraduate situations qualify for such loans. Parents get loans for the education of the student on the basis of attendance cost and their credit history. Just like the need-based loans, the Federal plus loans also carry low interest, and repayment is scheduled within 60 to 90 days after the full loan disbursement or after the completion of the course. Such a loan comes in handy in bearing other college expenses after using other financial aids.

4. Direct Consolidation Loans

This is not actually a loan but a facility. As the name suggests, it allows graduates to pool several loans into a single loan. It means the borrower has to make just one monthly payment. Moreover, it can help lower the monthly liability by extending the loan to more years.

5. Parent PLUS loans

Parent plus loan is a type of loan for biological, adoptive, and stepparents to support an undergraduate dependent on them. It is different from other loans in a way that the government expects parents to make the payment until the child is in school. However, one may request a deferment while applying for the loan.

The government does not offer a way for parents to transfer a PLUS loan to their children, but some private lenders do allow you to refinance a Parent PLUS Loan in a child’s name.

6. Private Loans

Students or parents with decent credit history can avail this kind of loan. The credit unions or the financial institutions that give such loans are authorized but not banked by the government. In case the student does not have a credit history, the guardian can apply for the loan, and the student has to be a co-signer.

Interest rates are comparatively higher on these loans. Therefore, such a loan is suitable for those who are confident of repaying even with a high-interest rate. However, there are some private institutions that offer lower interest loans for certain colleges.

One should opt for student loans from private institutions only when they do not get one from any Federal bank. Make sure that you understand all terms before availing of a loan from a private organization.

Tips to Compare Private Student Loans

As you prepare to get a private student loan, don’t wait for your school to decide how much of a loan you can handle: Do the due diligence yourself. Experts recommend borrowing no more than what you’ll most likely earn in your first year out of college. This can protect you from having unmanageable monthly payments after you leave school.

When you review each lender, consider the following factors:

- The amount you are able to borrow

- The overall cost of the loan, including its interest rate and fees

- When you must start repayment

- How long you have to repay the loan

- What help the lender offers if you have trouble affording your payments

- Your credit score; lower scores receive higher interest rates

- Available discounts, including autopay discounts

- If you can add a co-signer (and if you can qualify for a co-signer release later)

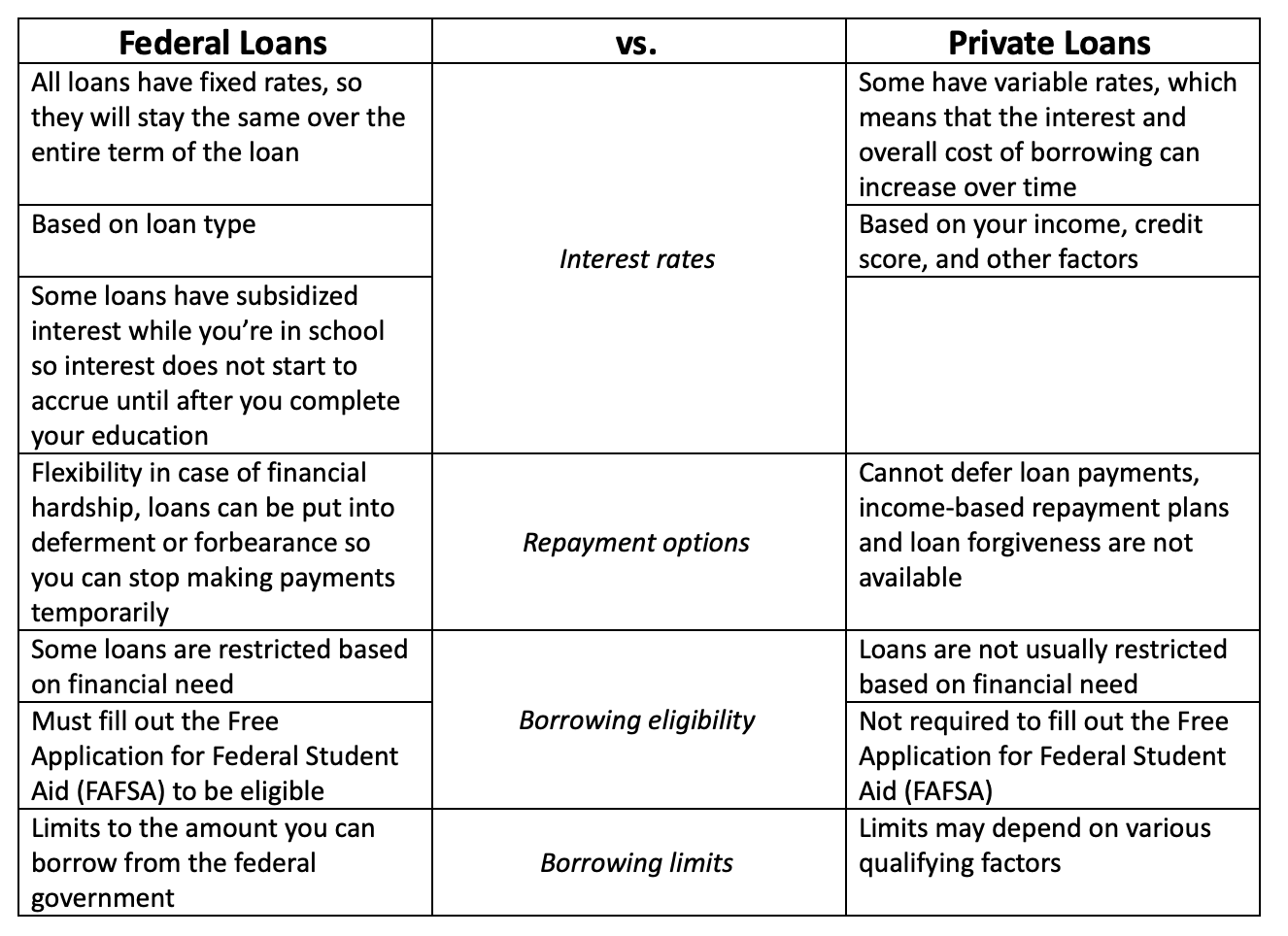

Comparing Federal Loans vs. Private Loans

The great majority of student loans are made through the William D. Ford Federal Direct Loan Program, but when students need more help to complete their college education, they turn to private lenders, such as banks or credit unions.

The major difference between federal student loans and private student loans is the cost and the use of credit scores in determining eligibility.

Undergraduate students applying for federal loans will not have to go through a credit check. Graduate students seeking federal loans must go through a credit check and could be denied loans if there is adverse information in their credit history.

Credit checks are the norm for public loans. A credit score of 640 or better is required and, depending on the terms and conditions, you may need a score much higher than that to be approved.

Other differences between public and private student loans include:

- Interest rates on federal loans are fixed. The interest rates on private student loans can be variable or fixed and usually are higher.

- Undergraduate borrowers who can demonstrate financial need could receive a federal subsidized loan, meaning the government pays the interest until you graduate. Private loans never are subsidized. You pay all the interest.

- Federal loans offer flexible repayment options and loan forgiveness programs. Some substantial portion of federal loans may be forgiven if Democrats in Congress have their way. Private loans have few repayment options, no loan forgiveness programs, and are unlikely to be included for amnesty in any federal legislation.

- Federal loans don’t have to be repaid until you graduate or drop below half-time status as a student. Many private loans ask for repayment while you’re still in school.

7. Refinanced Loans

Like consolidation loans, private lenders also offer an option to combine different types of student loans – Federal and private loans – into one loan. Such an option may not be a very good idea as it does not result in a saving. Such a type of consolidation would expand the repayment term and can increase the cost.

One advantage of refinancing is the lower interest rate that would convert into savings. But, a borrower will need a robust credit score and steady income to qualify for a lower interest rate. You would see many private lenders talk about the saving of an average customer through refinancing the loan.

Private lenders aren’t shy about promoting their average customer’s savings by refinancing. Although that number is important, consider whether you’re the type of borrower who is likely to match that success. It’s especially crucial to proceed with caution if you’re refinancing federal loans and would lose their associated protections and forgiveness programs.

How Do Student Loans Work?

Students and their parents can borrow either private or federal student loans to pay for higher education. These loans can be used to pay for many school-related expenses, including:

- Tuition

- Room and board

- Books and school supplies

- Transportation costs

- Technology equipment such as a computer or related software

- Food, utilities and other common living expenses

Your exact repayment terms will vary based on your lender, but most student loans don’t enter repayment until after the student has left school. You can usually select a repayment term between five and 20 years, though longer repayment periods usually come with higher interest rates.

Can I Get a Student Loan Without a Co-signer?

It’s possible to get a student loan without a co-signer, but the difficulty of doing so depends on your situation.

Nearly every type of federal student loan does not require (or allow) co-signers. Because you don’t need a high credit score to qualify for these types of loans, most students are eligible without a co-signer if they can meet a few basic requirements.

Private student loans, however, may be harder to get on your own. These types of loans require a high credit score of at least 670 to qualify for the lowest rates. If you can’t qualify individually, you may need to add a co-signer to your application. However, some lenders offer a co-signer release after you meet certain requirements, so look for that feature as you compare your options.

Some private lenders specialize in student loans without a co-signer; instead of reviewing your credit, they may consider things like your performance in school and field of study instead. While it may be easier to qualify for these loans, they typically come with higher interest rates.

How to Get Private Student Loans for Bad Credit

It’s possible to get private student loans with bad credit, but you’ll pay more for the privilege.

Some lenders offer student loans specifically for borrowers with bad credit or no credit. These loans have more relaxed eligibility requirements, and some don’t require a credit check at all. Instead, lenders may review alternative factors such as your field of study, grade point average or estimated future earnings to determine your eligibility. However, these loans come with significantly higher interest rates than traditional private student loans.

If you have bad credit, consider federal student loans first. Most of these loan types don’t check your credit, and the interest rates are standardized. That means everyone who qualifies for a federal loan receives the same interest rate, regardless of their financial history.

If you don’t qualify for federal student loans or have maxed out the federal aid available to you, consider taking steps to improve your credit before applying for a private student loan. If that’s not an option, you might add a co-signer to your loan application, which can help you qualify for better interest rates

CONCLUSION

Part of why private loan companies have enjoyed success in lending to students, graduates and parents alike is that they’re able to offer customized loans to creditworthy borrowers. Federal loans, on the other hand, were established to help cash-poor or credit-risky borrowers afford the rising costs of college.

Review all of these student loan types before deciding what’s best for you — and only you.

Leave a Reply